How to prepare for the expense of potential cognitive decline

The costs associated with an unhealthy brain can be significant. In addition to medical costs, other areas of expenses may include caregiving, medication, and housing needs. We’ll outline potential costs in each of these areas, but first, let’s define the difference between dementia and Alzheimer’s disease.

The difference between Dementia and Alzheimer’s Disease

Alzheimer’s disease and dementia are often used interchangeably, but they are not the same thing. Dementia is a general term that describes a group of symptoms affecting memory, thinking, and social abilities. It is a progressive condition that affects cognitive functioning, leading to a decline in memory, language, problem-solving, and other cognitive abilities.

Alzheimer’s disease is a specific type of dementia, accounting for about 60-80% of all cases. It is a degenerative brain disorder that gradually affects memory, thinking, and behavior. Alzheimer’s disease is characterized by the buildup of beta-amyloid plaques and tau protein tangles in the brain, which interfere with the communication between brain cells and eventually cause their death. Next, we’ll look at some trends related to the cost of an unhealthy brain.

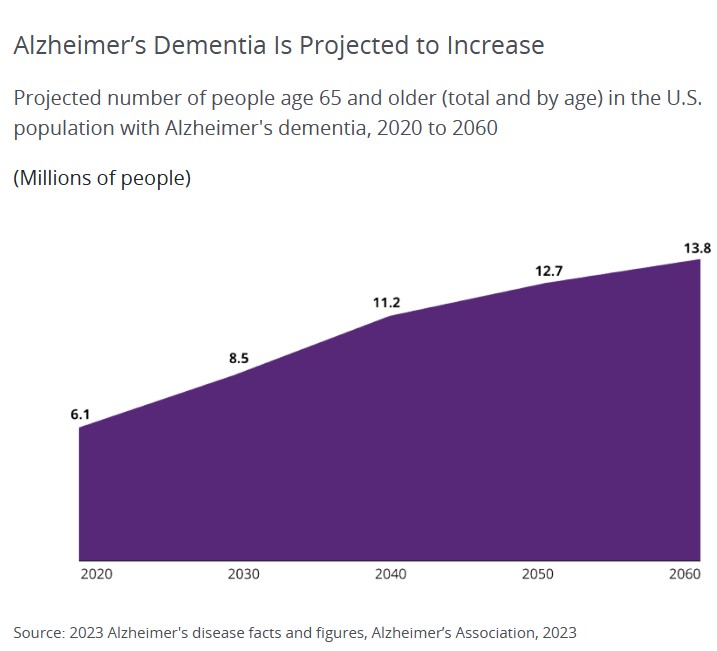

Trends of Dementia and Alzheimer’s Disease

- Alzheimer’s disease is on the rise (See graph below). Because increasing age is the predominant risk factor for Alzheimer’s dementia, as the number and proportion of older Americans grows rapidly, so too will the numbers of new and existing cases of Alzheimer’s dementia.

- People 65 and older survive an average of four to eight years after an Alzheimer’s diagnosis, yet some live as long as 20 years with the disease1

- Changes in the brain may begin a decade or more before symptoms appear

How Brain Health Affects Your Finances

The Financial Costs of an Unhealthy Brain

To understand the potential financial needs during the course of Alzheimer’s disease, we need to consider all the costs we might face now and in the future. Since Alzheimer’s is a progressive disease, the type and level of care needed will intensify over time.

The more financial planning that can be done soon after an Alzheimer’s diagnosis, the better prepared one will be for financial issues and expenses—especially while people can still make financial and caregiving decisions for themselves.

-

Medication

The cost of Alzheimer’s medications varies based on the type of drug, dosage, frequency, treatment duration, and patient location.A 2012 Consumer Reports study estimated that annual prescription costs for Alzheimer’s range from $2,124 to $4,800.

A newer drug, Aduhelm, does not cure the disease but may slow some debilitating symptoms. Its price is approximately $28,000 per year. Medicare usually covers 80% of medication costs. For Aduhelm, patients would pay $5,600 per year for the 20% not covered.Currently, Medicare limits coverage for Aduhelm to beneficiaries enrolled in clinical trials.

-

Caregiving

Initially, a person diagnosed with dementia can often live independently. Family and friends usually provide care during this stage.As the disease progresses, a home health aide may become necessary. These professionals help with basic daily activities and personal care. They can also assist with tasks such as shopping, cooking, or paying bills.

Home health aides provide more extensive care than family or friends typically can. They may help with bathing, dressing, grooming, preparing meals, administering medications, monitoring vital signs, and performing light housework.The annual cost for a home health aide working 44 hours per week is approximately $61,776.[4]

-

Housing

In the middle stages of Alzheimer’s, a person with dementia often requires 24-hour supervision to ensure safety. As the disease advances to the late stages, care needs become even more intensive.

Deciding to move a loved one into a long-term care facility, such as assisted living or a nursing home, can be very difficult. In many cases, it is not feasible to provide the necessary level of care at home.

The cost of long-term care facilities varies widely. It can range from $50,000 to over $150,000 per year, depending on the level of care and location.[4,5]

What Medicare and Medicaid Cover

What Medicare Covers

Medicare provides coverage for up to 100 days of skilled nursing care per illness. However, recipients must meet specific requirements before Medicare will pay for a nursing home stay. As a result, many Medicare patients are discharged from nursing homes before they are ready.

Important: Medicare does not cover long-term nursing home stays.[6]

What Medicaid Covers

Medicaid may pay for nursing home care for individuals who:

-

Require that level of care, and

-

Meet the program’s financial eligibility requirements.

Medicaid rules vary by state and by the marital status of the applicant. For those who qualify, Medicaid covers the full cost of nursing home care, including room and board.

Medicaid generally requires applicants to spend down most of their assets before coverage begins. Essentially, the program requires you to become “impoverished” under its guidelines. Once approved, Medicaid will cover care for as long as it is needed—even for the remainder of one’s life.[7]

The Total Lifetime Cost Dementia

The total lifetime cost of care for someone with dementia is estimated at $392,874 in 2021.8

These costs may include:

- Medical expenses: This includes doctor’s visits, hospitalizations, and medication costs.

- Caregiving costs: Dementia patients often require round-the-clock care, which can be provided either by family members or professional caregivers. This can be a significant expense, particularly if the patient requires skilled nursing care.

- Home modifications: As the disease progresses, patients may require modifications to their home to make it safer and more accessible. These modifications can include installing handrails, wheelchair ramps, and stairlifts.

- Lost income: Caregivers may need to reduce their work hours or stop working altogether to care for their loved ones with dementia. This can result in a significant loss of income.

- Legal and financial fees: As the disease progresses, patients may become unable to manage their own affairs. This can lead to legal and financial issues that require the assistance of an attorney or financial professional.

- Hospice and end-of-life care: In the later stages of dementia, patients may require hospice or end-of-life care. These services can be expensive and may not be covered by insurance.

From a financial standpoint, obviously, we’d all love to say there are things we can do to eliminate the risk of dementia, Alzheimer’s, and mental decline. While that may not be practical, if we could postpone the age at which it occurs, it would impact this number and, beyond the number, our quality of life. If there’s anything we can do to maintain a healthy brain as long as we can, we should be interested in doing that.

Steps we can take to prepare for the potential costs of cognitive decline for ourselves or a loved one:

Planning for Cognitive Decline

Cognitive decline, such as dementia, can lead to significant care costs. Preparing early can help protect your finances and ensure quality care for yourself or a loved one.

Start Planning Early

Even if your family has no history of cognitive disease, it is wise to think ahead. Anticipate potential costs and identify resources that may help cover them.

Consider Long-Term Care Insurance

Long-term care insurance can help pay for care if you develop dementia and need assistance with daily activities. Choosing a policy early can secure better coverage and lower premiums.

Protect Your Assets with a Trust

Setting up a trust can safeguard your assets and ensure they are used to pay for care. A trust gives you control over how your assets are managed, even if you cannot make decisions due to dementia.

Work with Financial and Legal Professionals

A financial advisor can help you plan for dementia-related costs. They can suggest investment strategies and retirement plans that account for potential long-term care expenses.

An elder law attorney can prepare essential documents, such as:

-

Durable power of attorney for finances

-

Durable power of attorney for healthcare

-

Living will

-

Trusts

These documents allow a trusted person to make decisions if you cannot manage your finances or healthcare.

Consider a Life Care Manager

A life care manager can guide you on financial planning specific to cognitive decline. They can also help coordinate care and ensure that your needs are met.

Communicate with Your Loved Ones

Have open conversations with family about your plans. Their support can help ensure your wishes are respected and reduce stress during challenging times.

Maintain Brain Health

Taking steps to maintain brain health—such as exercising, eating well, staying socially active, and challenging your mind—can help reduce the risk of cognitive decline and associated costs.

Source: Hartford Funds Investor Insight

1 Renata Pellegrino et al., “A Novel BHLHE41 Variant is Associated with Short Sleep and Resistance to Sleep Deprivation in Humans,” Sleep 37, no. 8 (2014): 1327–1336, https://doi.org/10.5665/sleep.3924.

2 Kazue Okamoto-Mizuno and Koh Mizuno, “Effects of thermal environment on sleep and circadian rhythm,” Journal of Physiological Anthropology 31, no. 14, (May 31, 2012), https://doi.org/10.1186/1880-6805-31-14.